FAQ

Budget and Financial Management

Q: Why isn’t all revenue included in the operating budget?

A: The operating budget includes general fund expenditures and revenue only to ensure transparency during public deliberation, and all related documents are posted online. The Town Charter references the general fund as the operating budget on page 124 (SECTION 10-2). Grants are approved by the Legislative Council in a separate process. While some grants (like CDBG and ARPA) allow budgeting for administrative expenses, these are approved separately by the Council and can decrease the use of local tax dollars. The Legislative Council receives detailed information about all grant expenditures as part of their approval process, as well as a listing of all grants received annually outside the general fund. Following best practices from the Government Finance Officers Association (GFOA), the Town accounts for grant financial transactions in segregated grant funds to properly manage and report expenditure for grant compliance.

Q: What is the general process of reviewing the department requests for the budget? Who manages and works on this process?

A: Department Heads budget for their needs and present these requests to the Mayor. The Mayor and the Mayor's office review these requests together, and the Mayor makes budget adjustments based on past actual spending, priorities, and the Town's needs.

Q: Over a six-year period, the Town budget has gone up 37% but the consumer price index (CPI) has only gone up by 25%. What specific actions have you taken to control spending and reduce the cost of government?

A: The current Mayor has been in office for 3 1/2 of those six years. Prior to this administration, the fund balance was negative. In addition to responsible budgeting, the current administration had to restore the fund balance as required by the State of Connecticut and right-size departments that were unable to operate effectively.

Q: Is the Fund Balance Low?

A: At the beginning of the Mayor's term, the fund balance was critically low; in fact, it was negative. This administration has grown the fund balance to over 7% of our operating expenses. The revenue from the sale of Wintergreen School was deposited into the fund balance and subsequently allocated to Capital Nonrecurring Funds for both the Town and the Board of Education to finance capital expenses. These funds are controlled by the Legislative Council, and with their vote, the Town has utilized the fund balance to fund certain operations and capital projects for both the Town and the Board of Education. The upcoming audit will demonstrate a fund balance exceeding 7% of operating expenses, and projections indicate that this level will be maintained above 7%. Within three months of her term, the Mayor submitted a fund balance policy to the Legislative Council, establishing a goal of maintaining 7% in the fund balance with the aspiration of increasing that amount. Given that our projections show the Town's fund balance will be approximately 7%, the Finance Department does not recommend the Legislative Council utilize the fund balance for FY26.

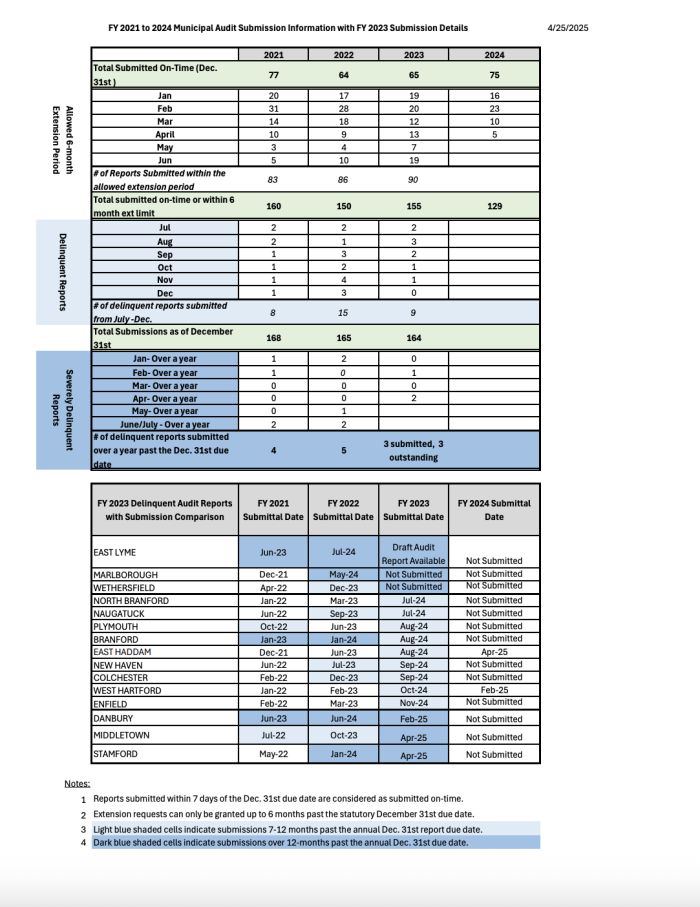

Q: Is the Audit Late, and How Can the Council Make Decisions?

A: The Office of Policy and Management (OPM) allows an additional six-month grace period before towns are considered out of compliance regarding their audits. The audit will be completed before this grace period expires, meaning Hamden is currently still in compliance. When preparing the budget, the Mayor bases decisions on five years of past actual financial data, the revenue and expense reports for the end of fiscal year 2023-2024, and the current year's financial experience. The Legislative Council can utilize this same data to inform their work. According to the OPM report of completed audits, 75 out of 169 municipalities had completed their audits by December 31, 2024, while 40 municipalities had outstanding audits.

Under normal circumstances, with a fully staffed finance department and all data readily available, completing an audit within six months after the end of the fiscal year is a challenging undertaking. The Finance Department has experienced a vacancy for our accountant position and has now been without a finance director for seven months. The new accountant is still becoming proficient in their role, and a candidate has accepted an offer for finance director, with a start date of May 30th.

Q: Was $12.6 Million in Salaries Improperly Covered by Federal Funds?

A: This assertion reflects a significant misunderstanding of grant management and municipal finance as it pertains to our FY 24 budget. As the deadline for obligating ARPA funds on December 31, 2024, rapidly approached, our Grants Director identified several Legislative Council ARPA projects that were at risk of not being obligated on time or of missing the expenditure deadline of December 31, 2026. To secure these funds and ensure their obligation, thereby preventing the potential loss of millions of dollars, the Legislative Council obligated the projects as allowable municipal expenses under ARPA guidelines. Subsequently, the Legislative Council voted to place the same amount in restricted funds based on the priorities outlined in the Legislative Council’s ARPA budget. This was not a case of concealing a surplus but rather a strategic move to safeguard and appropriately allocate federal funds according to ARPA regulations and the Council's directives.

Q: Was $5 Million in "Fake" Red Light Camera Revenue Included in the Budget?

A: During the public budget deliberations last year, we discussed the implementation of red light and speed enforcement cameras, and we outlined the necessary steps involved. These steps included drafting and passing an ordinance to authorize the cameras and the Town's ability to issue fees and collect revenue, issuing a Request for Proposal (RFP) to procure a vendor, and negotiating a contract with the selected vendor. The contract negotiation phase proved to be the most time-consuming, as our priority was to ensure the protection of Hamden residents throughout the process. The Legislative Council has since approved the contract. Our Traffic and Engineering Departments have provided crash data, traffic counts, and specific intersection information to the vendor, who is now compiling reports for submission to the Connecticut Department of Transportation (DOT). The next stages involve DOT approval of the locations, vendor installation of the cameras, and their activation. Following a 30-day warning ticket period, we will be able to issue fees. We are nearing the completion of this process, currently approximately three months behind the initial schedule.

Q: Was $7.8 Million Claimed as "Spent" but Never Touched?

A: Last year, the budget included $7.8 million from the fund balance with the intention of returning these savings to taxpayers. Throughout all of our public budget deliberations, our commitment was to utilize this $7.8 million in June, if necessary. We currently anticipate needing these funds next month to finalize the fiscal year. Therefore, the money was not claimed as "spent" in the sense of being already disbursed, but rather it was identified as a potential revenue source to be used at the end of the fiscal year to realize savings for taxpayers.

Q: Several departments were given increases in this proposed budget that outpace the CPI. Why did you propose these numbers?

A: Most of the proposed budget increases are based on contractual obligations. The Board of Education also has contractual obligations approved by the BOE and Town Council, such as the Teachers' contract and the Transportation contract. Additionally, proposed changes by the Governor regarding special education may require increased funding to prepare for educating more special education students within the district, which could ultimately benefit Hamden.

Q: Please explain why the budget includes line items increasing more than 3%, such as the Legislative Council, Registrar of Voters, HR, Purchasing, Senior Services, Culture Affairs, Animal Control, Traffic Department, Engineering Dept.

A: Historically, the Legislative Council has maintained $1 million in the Emergency and Contingency line. This has been reduced to $300,000. While Finance recommends a 1% contingency (which would be $3 million), the proposed budget increases this line to $500,000, which is still considered a responsible but lower amount than recommended. The current and proposed budgets are based on an ideal scenario, which is unlikely to occur.

Q: Why are you proposing a mill rate that will functionally raise taxes for most Hamden homeowners, and why aren’t all the additional proceeds going toward debt reduction rather than operational spending?

A: The presented budget reflects the necessary funding to meet the Town's current operational obligations. To allocate more funds towards debt reduction would necessitate a larger tax increase. Each year, the Town allocates funds towards paying down Other Post Employment Benefits (OPEB), which represents the largest liability.

Q: Why are we spending money on "nice to haves" in the capital expenditures (new snow plows, dump trucks, ice rink upgrades, etc.) when the town is financially struggling?

A: Vehicles for Public Works are not considered "nice to haves." The Town has trucks with detached frames due to the corrosive effects of road salt, and the Police, Fire, and Public Works departments all have aging fleets. The vehicle repair line is struggling to keep up with breakdowns. These vehicles are essential for providing public safety services. Prior to the current administration, vehicle replacements were not consistently made, contributing to the current state of disrepair. A gradual update of the fleet is necessary to ensure the Town can maintain normal operations and respond to emergencies effectively.

Q: How much would closing the two small libraries save?

A: Closing the two branch libraries would result in savings of approximately $40,000-$60,000 in utilities and materials. There are also four employees between the two branches whose salaries would be a factor in total savings.

Q: Is it true that Public Works went up $40 million? What’s behind this increase?

A: This is incorrect. The Public Works budget is proposed at $14,708,806, compared to the current budget of $14,109,503.

Q: The budget assumes a 3% tax revenue increase every year for the next 5 years. How is this happening? Is the plan to continue raising the mill rate every year until it returns to the mid-50s?

A: A 3% growth in tax revenue is considered a reasonable expectation to cover contractual increases. The administration is focused on economic development, engaging with real estate developers, property owners, and businesses to encourage development on undeveloped land and improved use of existing properties. Enhancing commercial properties and increasing affordable housing contributes to the grand list, which can help shift the tax burden back to commercial properties during the next revaluation, rather than relying solely on mill rate increases.

Q: Why is the BOE not being flat-funded in this budget? Should they not also do more with less?

A: The Board of Education has contractual obligations that must be met. The student population increased during the pandemic, and while teaching and administrative staff have been reduced since then, significant contractual obligations remain, such as transportation, special education, and union and vendor contracts. Additionally, potential federal education funding cuts could further strain the BOE's budget. Flat funding would equate to a significant reduction given these unavoidable expenses. Hamden's public schools are also a key reason why many people choose to live in the town.

Q: How will the community center, which no one seems to want, affect the budget as an ongoing recurring expense?

A: The construction costs for the youth center were budgeted for with ARPA funds. Property taxes will not fund the construction or operating costs for the youth center. Current employees from a different building would staff the youth center. The Mayor has met with several groups of students who are enthusiastic about the youth center and have provided input on its features.

Q: How much are we spending on "nice to haves" like community centers when the town is struggling financially?

A: The community space at the Plaza is donated and has no operating budget impact. The Youth Center is funded by ARPA (American Rescue Plan Act) funds, which are separate from the operating budget that determines the mill rate. The budget presented to the Legislative Council does not include any new initiatives funded by local taxes.

Q: Are we taking a proactive approach in making significant cuts during the ongoing negotiations for police and other union contracts?

A: The Town's priority in all contract negotiations is healthcare savings. Medical expenses are a significant part of the budget at $57 million and contribute to a large Other Post Employment Benefits (OPEB) liability of $600 million. The Fire Department is currently operating at minimum manning levels to avoid excessive overtime. Reducing staff further could lead to increased overtime costs. Effective leadership within the Police and Fire departments is also focused on controlling costs.

Q: Why did you elect to do the assessments in 2024 instead of 2025, was that a strategic move to make it look like the mill rate was going down while also effectively increasing revenue to cover the deficit?

A: The State of Connecticut mandated the year for each municipality's revaluation to even out the workload for assessors and prevent price increases due to high demand. The 2024 revaluation year for Hamden was not a local decision. The schedule for each municipality is posted by the State: https://portal.ct.gov/-/media/opm/igpp-data-grants-mgmt/revaluation/revaluation-schedule.pdf?rev=c899c1af75454914b66d20682e071661&hash=0AE94A736939BFA9BC8512B25E227689

Q: Why are certain revenue streams missing from the budget like grants?

A: The operating budget does not include grant revenue. Grants are managed separately and supplement various Town functions. This separation allows the Town to track expenses for grants management and reporting. For example, a Police Department grant for "Click It or Ticket" funds officer overtime specifically for that initiative and is not part of the general operating budget. Some Police Department grants also offset fringe benefits like medical and pension costs.

Q: Why is the handling of ARPA money not transparent?

A: Both the Legislative Council and the Mayor held public meetings to gather suggestions for the use of ARPA funds. The formation and votes regarding the ARPA budget occurred during public Legislative Council meetings.

Q: Why are fund balances not being disclosed to the council?

A: The Legislative Council received a fund balance report during their budget meeting on April 19, 2025.

Q: How did you grow the fund balance to improve our bond rating? Did that cause other problems that are contributing to the issues we are facing?

A: The fund balance was increased through a fund balance restoration plan initiated by the previous administration. This plan included restructuring debt, which extended the repayment period to create budget savings in the earlier years. These savings were added to the fund balance. This debt restructuring has contributed to the Town's current large debt service payments. The Town also achieved budget surpluses through strong collections of back taxes, salary savings from vacant positions, and medical cost savings.

Q: Why did you ignore the advice of the finance commission last year?

A: The Finance Commission provided a report to the Legislative Council disagreeing with the use of fund balance in the budget. This difference in opinion regarding the appropriate use of fund balance is not uncommon in many municipalities, as it can be a useful budget tool when a surplus is anticipated.

Financial Oversight and Accountability

Q: Why weren't up-to-date financial documents completed and given to the Legislative Council? They can't do their work without knowing exactly what was spent and what wasn't.

A: The Legislative Council has access to monthly revenue and expense reports that detail budget expenditures. These reports are also posted on the Town's website for public access. https://www.hamden.com/296/Financial-Information

Q: Why wasn't an audit completed in September and why wasn’t the council notified of the extension?

A: The audit is due December 31 to the Office of Policy and Management. The Council was informed that the audit was running behind schedule. The Town hired a new accountant last year, and this is their first time preparing the audit, a significant undertaking that typically takes six months under normal circumstances. The Deputy Finance Director is training the new accountant while also managing their regular duties. Additionally, the Town has a new audit firm that requires all information to be uploaded, unlike the previous auditor who had historical data on file. The audit was also started late due to contract negotiations with the new firm, which is contracted by the Legislative Council.

Q: Why was it more than 3 months before the Financial Director position was posted after the former director left? Why has the Finance Director position remained unfilled?

A: The former Finance Director left on November 1, 2024. The job opportunity was posted on October 18, 2024, prior to the director's departure. The delay in filling the position involved negotiations with the Legislative Council to agree on a salary that would attract an experienced candidate. We are negotiating with the Legislative Council to bring in a qualified candidate.

Q: By what date do you plan to close out the previous fiscal year, provide the necessary information for auditors to complete the audit, and release this to the public?

A: The trial balances have been uploaded to the new auditor, Marcum, to begin the audit process. The Town is also working with the former auditor, Clairmont, to upload the necessary working papers. Weekly meetings are being held with Marcum, and the expectation is that the audit will be completed by the end of May.

Q: What specific steps will you take to prevent these financial delays from happening again in the future?

A: The Town's accountant is now trained and is already reconciling monthly statements for the next audit. A three-year contract is in place with the new auditor, Marcum, which will allow for the carryover of information, streamlining the process for future audits and ensuring they are completed on time.

Q: The Town Charter requires monthly financial reports to the Legislative Council. These have not been forthcoming. When will the Town comply with Charter requirements?

A: The Legislative Council has access to monthly revenue and expense reports that detail budget expenditures. These reports are also posted on the Town's website for public access. https://www.hamden.com/296/Financial-Information

Q: Why did the deputy finance director make $300k in 2023, which is far above anyone else in the town?

A: The Deputy Finance Director has extensive experience and capability. They often step in to cover vacancies and assist in training new employees. It is challenging to bring in external candidates who immediately possess the necessary understanding of the Town's financial systems.

Taxes and Taxpayers